Expansion

Structure supports risk

Normal exposure context.

Regime Atlas is a daily TradingView risk-authorization layer that shows whether market structure supports normal, reduced, or defensive exposure.

Validated across 31 instruments and 181,509 daily bars.

Drawdown reduced on 26/31 long tests and 30/31 short tests.

Win rate stayed broadly flat across regimes — Core does not predict direction. It classifies structure.

Most drawdowns are not entry problems — they are regime problems. A valid setup can still be a bad trade in the wrong environment. Regime Atlas classifies the environment before you deploy your strategy into it.

I built this after watching technically correct entries fail repeatedly inside structurally weak tape.

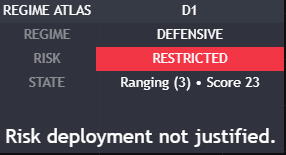

Four daily classifications, published after the daily close.

Regime — Expansion · Transitional · Fragmentation

Risk Tier — Authorized · Conditional · Restricted

Market State — Trending · Ranging · Transitional

Score — 0–100 structural alignment. Higher = cleaner alignment, lower = weaker or more hostile structure.

Core classifies the structure. You still choose the setup, direction, entry, stop, and exit.

Normal exposure context.

Reduced / selective exposure.

Defensive / restricted exposure.

You want long/short calls, copy-trade alerts, win-rate guarantees, or a magic button. Founding seats are for traders with an existing process who want structural exposure context around it.

No buy/sell calls. No long/short forecasts. No AI bias engine. No bundled dashboards or chat rooms.

I won't pretend to know where price goes next. The model doesn't either. It only asks whether the structure is worth deploying risk into.

Core was reviewed as a structural risk-authorization layer. The full Validation Brief is delivered after application so serious prospects can review the model in context.

Across equity indices, crypto, FX, commodities, and rates/bonds where applicable.

Current Fase 4 review set. Source of truth: 21 April 2026, 18:26 UTC.

Drawdown reduced on 26 of 31 long tests.

Drawdown reduced on 30 of 31 short tests.

31 assets, 181k+ daily bars. The founding-member brief names the worst regime calls too, not just the good ones.

The value is not one individual indicator. It is the proprietary classification framework that combines multiple structural dimensions into one daily regime output.

Each dimension is evaluated through a proprietary combination of fixed structural calibration and asset-relative context.

The inputs produce a composite regime classification with stability controls designed to reduce unnecessary regime flipping.

Exact lookbacks, formulas, constants, weights, thresholds, and classification parameters remain proprietary. The methodology and outputs are explained openly; the implementation details are not.

Regime Atlas is built by an independent trader-builder focused on market structure, regime classification, and risk authorization.

This is not a fund, not a signal service, and not a chat room. It is a daily classification layer for traders who already have a setup and want better regime context around exposure.

For traders who want a daily risk-authorization layer without signals, chat rooms, or execution automation.

After the first 10 seats, the next 15 seats open at €99/mo, locked for 12 months. No signals, no predictions, no performance claims.

No. Once a daily bar closes, the classification is not revised.

No. You keep your entries, exits, instrument selection, and directional bias. Regime Atlas provides exposure context around that process.

Check the table after the daily close. Regime, risk tier, state, and score before your next session.

No. It does not output long/short calls, entries, exits, alerts, or copy-trade instructions.

Because Core is designed to classify structure, not intraday noise. D1 keeps the output stable and repeatable.

The next 15 founding seats open at €99/mo, locked for 12 months. Existing €79/mo founding seats keep their lifetime price lock while subscribed.

The public validation summary is available here: Regime Atlas Core validation summary.

The public invite-only script page is available here: Regime Atlas Core Model on TradingView.

Regime Atlas Core is invite-only. The application helps confirm fit before payment instructions and TradingView invite steps are sent. If it looks like a fit, you will receive the next steps within 48 hours.